On This Page[Hide][Show]

Reliance Standard is a leading provider of employee benefit solutions, including a full range of short and long-term disability benefits. Founded in 1906, Reliance Standard Life Insurance Company is a member of the Tokio Marine Group, a multinational insurance holding company. Unfortunately for claimants, Reliance Standard Disability claim denials are far more common than approvals.

If Reliance Standard has denied your disability claim, contact us for a free case review. A disability lawyer from our firm can review your denial letter and guide you through the administrative appeal process with Reliance Standard Life Insurance Company. If necessary, we can also help you file a lawsuit against Reliance Standard Life Insurance Company.

The Reliance Standard Disability Claim Review Process

Once you file a claim for Reliance Standard disability insurance benefits, a disability claims representative will review your claim. They may contact you and request information about your activities of daily living, self-reported symptoms, and the facts and circumstances of any other disability claims you may have filed with another insurance company or the Social Security Administration.

Contact Information for New Claims

You can use the contact information below to submit your Reliance Standard disability claim to the insurance company:

Reliance Standard Life Insurance Company

PO Box 8330

Philadelphia, PA 19101-351-7500

Reasons Why Reliance Standard Denies Disability Insurance Claims

It is not uncommon for Reliance Standard to unfairly deny long-term disability claims. Reliance Standard has earned a reputation for denying claims by any means necessary.

You (Allegedly) Do Not Meet the Definition of Disabled

Recently, Reliance Standard has received media attention for its position in a recent lawsuit. The case involves an individual who, after enduring prolonged COVID-19 symptoms, was unable to work and subsequently had his disability claim denied. The company denied the claim, claiming that the individual did not meet their policy’s criteria for being “disabled”. The company is notorious for pushing claimants into litigation, especially in ambiguous cases. It takes an uncompromising stance on emerging issues such as COVID-19.

Exclusions and Limitations

Reliance Standard has also been known to misapply the pre-existing condition exclusion to deny claims at the outset or terminate a disability claim after 24 months. Reliance Standard may use one of several standard policy provisions to justify a claim denial at the two-year mark. Claims for certain mental or pain disorders, self-reported conditions, and even some musculoskeletal disorders are often limited to 24 months.

A Change in the Definition of Disability

Another common occurrence at the two-year mark is a change in the definition of the term “total disability” or “disabled”. Under most policies, Reliance Standard initially defines disability as the inability to perform one’s own occupation. However, after 24 months of benefits, Reliance Standard will define disability as the inability to perform any occupation.

How to Avoid a Long-Term Disability Claim Denial

Meet Your Policy’s Definition of Disability

There are no specific laws that determine what is or is not considered a disability for long-term disability claims. The term “disability” is defined in your disability insurance policy. The following policy excerpt is from a published court opinion involving a policy issued by Reliance Standard. However, it is best to look at your policy to determine the exact definition of disability that Reliance Standard will use to evaluate your disability claim.

“As defined by the policy, to qualify for disability during the initial 24-month period of coverage, an Insured must demonstrate an inability to perform material duties of her regular occupation.

To qualify for benefits after 24 months, a claimant must be unable to perform the duties of “any occupation,” which is defined as an inability to perform the material duties of any occupation that her education, training, or experience reasonably allow.

In addition, under the Mental or Nervous Disorders Limitation, benefits are not payable beyond 24 months for any disability that is caused by or contributed to by a mental disorder, including anxiety and depression.”

Submit All Medical Records Supporting Your Disability Claim

A claims examiner and a reviewing physician within the insurance company will review your disability claim, and both may selectively sift through your medical records to find information that justifies denying your claim. It is critical to provide a comprehensive set of medical records, including detailed results from diagnostic tests such as MRIs or CT scans, to protect against this selective review.

In addition, it is important that your physician and any treating specialists document the specific limitations resulting from your injury or disability. If you provide thorough documentation, it will be much more difficult for the insurance company to find a reasonable basis for denying your claim.

Be Prepared For Video and Social Media Surveillance

Reliance Standard has significant resources and will likely hire a private investigator to uncover any activity inconsistent with your disability claims. Investigators may use background checks and photo and video surveillance. They have also been known to monitor your social media profiles. They want to “catch” you doing something you “shouldn’t” be doing, like carrying a trash bag or enjoying time with your family.

It would help to be mindful of your activities and what you share on your social media profiles. However, everyone has “good days,” and an insurer may catch you on one of your more active days. An attorney can help you show that a brief period of activity on one of your best days does not indicate that you can return to work.

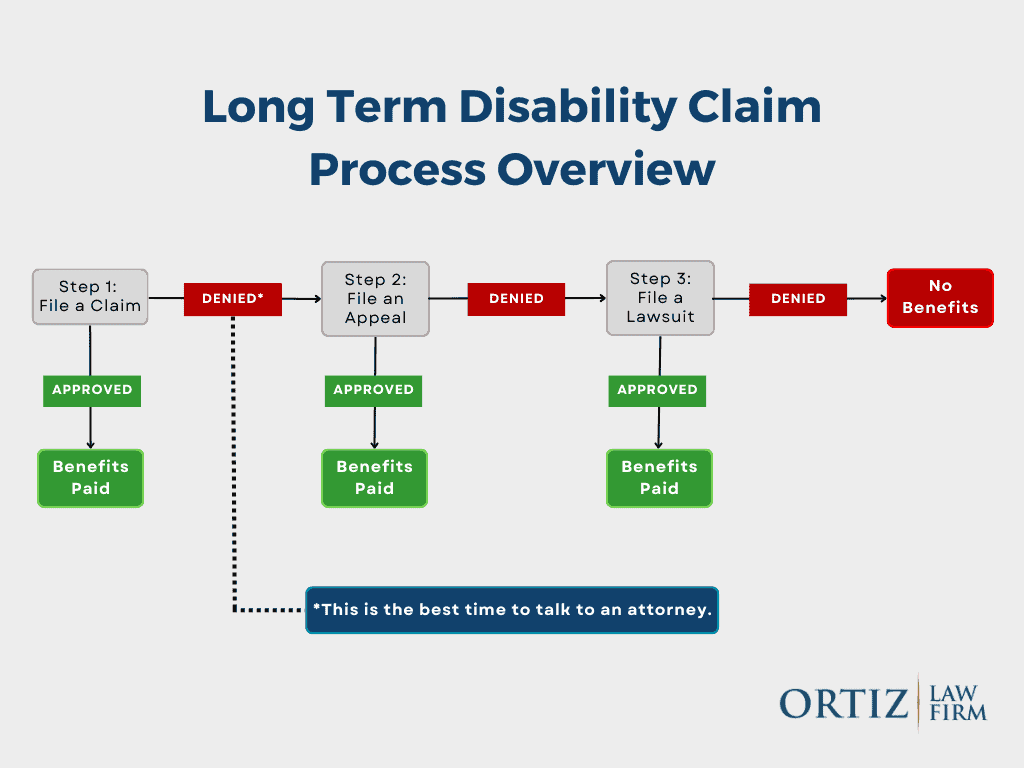

The Reliance Standard Appeals Process

If Reliance Standard denies your disability claim, the next step is to go through the insurance company’s internal appeals process.

When you go through the appeals process, Reliance Standard typically uses third-party medical reviewers to help process your long-term disability claim. These third parties are supposed to conduct an “independent” medical examination or file review to determine your eligibility for long-term disability benefits.

However, there is little evidence that these so-called independent doctors base their findings on proper medical criteria. It is common for doctors hired by Reliance Standard to discount or disregard the disabling effects of pain, fatigue, medication side effects, and even the opinions of your treating physicians in order to deny claims.

How Can a Lawyer Help If My Claim Is Denied?

Because the appeals process is so restrictive, we recommend that you request a free case evaluation before moving forward. An experienced long-term disability attorney can help you navigate the complex rules and regulations of ERISA. They will ensure that you understand your policy and ERISA laws, help you navigate the administrative appeal process, and fight for your rights in a lawsuit against Reliance Standard.

Understanding Your Coverage

The most important document in the entire process is the disability insurance contract, which defines the type of coverage Reliance Standard provides and the duties and responsibilities of all parties to the contract (i.e., the claimant and the insurance company). They are usually very complex and difficult to understand.

In addition, long-term disability insurance policies are often subject to change and are written in favor of the insurance company. The disability policy governs the type of coverage provided by a disability insurance policy, so we will make sure you understand the terms of your policy.

Determining If You Need to Appeal

For some policyholders, such as those with an individual disability insurance, an internal appeal may not be necessary . ERISA law does not apply to these policies, so you may not be required to appeal before filing a lawsuit. An experienced ERISA disability attorney can help you determine whether ERISA applies to your long-term disability claim.

Gathering Additional Evidence

We make sure we maximize the chances of overturning the denial of your disability insurance claim. We obtain additional medical and vocational evaluations. We use customized residual functional capacity forms to support your claim. We do the heavy lifting to gather evidence that supports a favorable disability determination so you can focus on your health.

Appeals and Litigation Preparation

If your claim is denied, the most important thing you can do is prepare a strong appeal. This is essential not only to overturn a denial, but also to strengthen the administrative record in case you need to file a lawsuit. If you file a lawsuit, the court will only review the medical records submitted during the administrative review process.

When you hire the Ortiz Law Firm to represent you as your attorney for an administrative appeal, we will obtain a copy of your claim file and policy, conduct a medical review, and evaluate all of the medical records and vocational evidence considered by Reliance Standard Disability Insurance Company.

We won’t give up until we get you the long-term disability benefits you deserve. When your administrative appeals are exhausted, we can help you file a lawsuit against Reliance Standard. We always work on a contingency fee basis for our clients, so you do not have to pay any court fees up front.

ERISA Law and Your Long-Term Disability Claim

The Employee Retirement Income Security Act, a federal law, governs most employer-sponsored long-term disability plans. Federal Employee Retirement Income Security Act (ERISA) laws heavily favor insurance companies like Reliance Standard and are not consumer friendly to individual claimants.

Under ERISA, you generally have 180 days after receiving of your disability insurance claim denial to submit information to support your disability claim. This evidence is critical, and that’s because a federal court generally will not accept or consider new evidence presented during litigation.

Remember, the court is limited to seeing what was in the administrative record when the insurance adjuster decided your long-term disability claim. You or your attorney should submit all relevant evidence and documentation supporting your disability claim to the insurance carrier or plan administrator with the initial administrative appeal.

FREE RESOURCE: Check out our step-by-step guide to appealing a disability insurance claim denial. The guide includes instructions and appeal templates for ERISA and non-ERISA claims.

Lawsuits Against Reliance Standard Life Insurance Company

If Reliance Standard denies your administrative appeal, or if Reliance Standard denies your initial claim and you have an individual policy that is not governed by ERISA, you may be able to file a lawsuit against Reliance Standard for denying your claim.

It is important to have a skilled attorney who understands ERISA appeals and lawsuits to defend your case. Reliance Standard has its own ERISA attorneys and strategies for success in federal disability lawsuits. It would be best to have an ERISA disability attorney on your side to help you strengthen your claim, which means retaining an attorney before you even file your appeal.

Reliance Standard Case Summaries

Below are several examples of litigation against Reliance Standard. We did not handle these lawsuits, but have summarized them to help plaintiffs better understand how federal courts interpret disability law.

- Senegal v. Reliance Standard – Court Remands Case for Further Review

- Okuno v. Reliance Standard – Court Rules in Favor of Reliance

- Lash v. Reliance Standard – Court Dismisses Case for Failure to State a Claim Against Matrix

- Coats v. Reliance Standard – Court Finds Calculation of Benefits Incorrect

- Killen v. Reliance Standard – Court Finds No Abuse of Discretion

- Bradshaw v. Reliance Standard – Pre-Existing Condition Exclusion Incorrectly Applied to Claim

- Bey v. Reliance Standard – Court Finds Reliance Did Not Act Arbitrarily or Capriciously

- Bowman v. Reliance Standard – Court Finds Denial Was Not Arbitrary & Capricious

- McIntyre v. Reliance Standard – Court Finds Claimant Disabled Under Any Occupation Standard

- Craft v. Reliance Standard – Reliance Committed Abuse of Discretion

How the Ortiz Law Firm Can Help

Filing for Reliance Standard Disability Benefits

If you are preparing to file a claim for long-term disability benefits, we have a Disability Insurance Claim Guide and Toolkit to help you through the process. This free resource will guide you through the process and help you gather the information you need to support your claim.

We also have a free eBook called the “Top Ten Mistakes That Will Destroy Your Long-Term Disability Claim“. Read this book to avoid common mistakes that can destroy your claim.

Appealing a Reliance Standard Disability Claim Denial

When your insurance company refuses to pay your disability benefits, an experienced ERISA attorney at the Ortiz Law Firm can help you get the benefits you deserve. Many of the Reliance Standard claims we handle are approved on appeal. The following are just a few of the claims we have brought to a favorable resolution.

- Claim approved for benefits under the “any occupation” definition of disability: After nearly eight years of paying benefits, Reliance Standard conducted a full file review with a vocational expert and concluded that the available information did not support an inability to perform “any occupation.” We appealed, and Reliance Standard ordered a peer review report. The report supported the decision to terminate benefits, but we argued that the doctor had ignored the claimant’s need for “frequent unscheduled breaks.” Reliance Standard then reversed its decision to terminate the claim.

- Claim reinstated after termination due to policy’s mental health limitation in policy: Reliance Standard initially denied our client’s long-term disability claim because he had been terminated. We appealed, arguing that his disability began before his termination, and the denial was overturned. The claim was paid for two years and then terminated due to a policy provision limiting benefits for mental health conditions. We appealed again and proved that our client was still disabled due to frequent headaches, chronic neck and back pain, and chronic fatigue.

We have a “No Recovery, Zero Fee Guarantee.” This means our clients only pay a fee when disability benefits are recovered.

If Reliance Standard is denying your claim for long-term disability benefits, the disability lawyers at the Ortiz Law Firm can help. Disability attorney Nick Ortiz represents disability insurance claimants throughout the United States. Let us fight for the Reliance Standard disability benefits you deserve. Call us at (888) 321-8131 to request a free consultation with a disability attorney.