Table of Contents[Hide][Show]

- What Is Metabolic Syndrome X?

- How to Build a Strong Disability Claim for Metabolic Syndrome X

- The Appeal Process: Don’t Give Up After a Denial

- Why You Need an LTD Attorney for a Metabolic Syndrome Claim

- Frequently Asked Questions About Long-Term Disability and Metabolic Syndrome X

- Take the Next Step Today

If you’ve been denied long-term disability (LTD) benefits because of metabolic syndrome X — also called insulin resistance syndrome — you are not alone, and you are not without options. Insurance companies routinely deny these claims, often by downplaying the severity of the condition or arguing that it is manageable with lifestyle changes. But metabolic syndrome is a serious, complex disorder that can leave people genuinely unable to work. Here’s what you need to know about your rights, your medical evidence, and your path forward.

What Is Metabolic Syndrome X?

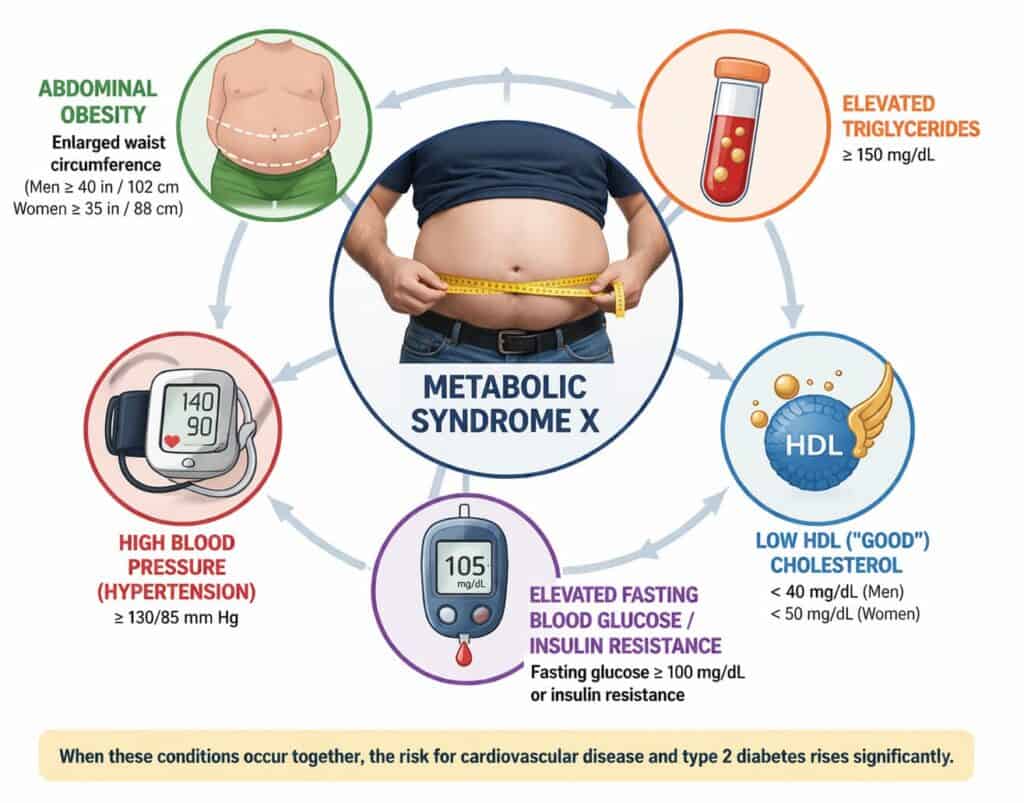

Metabolic syndrome X (also known as Syndrome X, insulin resistance syndrome or metabolic syndrome) is not a single disease — it is a cluster of interconnected metabolic conditions that dramatically increase the risk of cardiovascular disease, Type 2 diabetes, and stroke. To be diagnosed, a person typically presents with at least three of the following five markers:

- High blood pressure (causing daily headaches and brain fog)

- High blood sugar (triggering extreme afternoon fatigue)

- Large waistline (adding constant physical strain)

- Low HDL cholesterol (impairing recovery)

- High triglycerides (compromising blood flow and draining energy)

Together, these conditions create a compounding burden on nearly every major organ system. Research published in Scientific Reports found that metabolic syndrome was directly associated with higher rates of functional dependence in daily activities, mobility limitations, and general physical activity impairment. The more components a person has, the more severe their disability is likely to be.

This is not a condition you simply “walk off.” For many claimants, metabolic syndrome causes chronic fatigue, cardiovascular complications, neuropathy, difficulty standing or walking for extended periods, cognitive difficulties, and secondary conditions such as sleep apnea, kidney disease, and depression — any of which can individually prevent a person from sustaining full-time employment.

Why Insurers Deny Long-Term Disability Claims for Metabolic Syndrome

Insurance companies have a financial incentive to deny claims, and metabolic syndrome X gives them several convenient arguments to do so. Understanding their tactics is the first step toward defeating them.

“Your Condition Is Manageable”

Insurers often argue that with diet, exercise, and medication, metabolic syndrome is controllable — and therefore not disabling. This ignores the reality that many claimants have already attempted lifestyle interventions, and still suffer from serious, ongoing functional limitations. The cumulative damage to the cardiovascular system, kidneys, and other organs is often irreversible.

“There Is Insufficient Medical Evidence”

Because metabolic syndrome involves multiple overlapping conditions rather than a single dramatic diagnosis, insurers may argue that no single piece of evidence proves total disability. They frequently claim that diagnostic tests, physician statements, or treatment records are inadequate — even when the combined picture clearly shows someone who cannot sustain full-time work.

“The Symptoms Are Self-Reported”

Some LTD policies limit or exclude coverage for “self-reported” conditions. Insurers may try to categorize fatigue, pain, or cognitive difficulties associated with metabolic syndrome as subjective and unverifiable, even when these symptoms are clinically documented.

How to Build a Strong Disability Claim for Metabolic Syndrome X

Winning a long-term disability claim for metabolic syndrome requires a comprehensive, well-documented approach. Here is what you need to establish:

- Document Every Condition Separately and Together: Metabolic syndrome’s power — and its challenge in a disability claim — is that it involves multiple conditions interacting with one another. Work with your treating physicians to document each component individually (hypertension, blood glucose levels, lipid panels, cardiovascular findings) and how they combine to limit your functional capacity. An insurer who dismisses one condition in isolation may have a harder time ignoring the compounding effect of four or five.

- Obtain a Detailed Functional Capacity Evaluation (FCE): A Functional Capacity Evaluation objectively measures your ability to sit, stand, walk, lift, carry, concentrate, and sustain activity over time. It translates your medical conditions into the language insurers and courts understand: can you do your job, or any job, for a full workday on a sustained basis?

- Get a Thorough Attending Physician Statement (APS): Your doctor’s opinion matters — but a vague statement is nearly useless. You need a detailed Attending Physician Statement that explains not just your diagnoses, but exactly how your conditions prevent you from performing your occupational duties. Ask your physician to describe your specific functional limitations, the objective findings that support them, and the expected duration of your disability.

- Gather Comprehensive Lab Work and Test Records: Lab results are the backbone of a metabolic syndrome claim. Cholesterol and lipid panels, blood glucose and HbA1c tests, blood pressure readings over time, and any cardiac imaging or stress test results should all be included. These are the objective findings that validate the presence and severity of your condition.

- Keep a Symptom Journal: A daily symptom journal is a simple but powerful tool that many claimants overlook. Record how your condition affects you each day — your energy levels, pain, ability to sit or stand, cognitive difficulties, and any tasks you were unable to complete. Over weeks and months, this creates a contemporaneous, detailed account of your functional limitations that is difficult for insurers to dismiss. It also helps your physicians write more accurate, specific statements on your behalf.

- Document Secondary Conditions: Metabolic syndrome frequently causes or exacerbates other disabling conditions. Sleep apnea, neuropathy, cardiovascular disease, kidney dysfunction, and depression are common secondary diagnoses that can independently support a disability claim — or combine with the primary syndrome to satisfy a medical listing or overwhelm a residual functional capacity assessment.

The Appeal Process: Don’t Give Up After a Denial

A denial letter is not the end. In fact, for most employer-sponsored disability plans, appealing the denial is a critical step — and missing the appeal deadline can permanently forfeit your right to benefits.

Under the Employee Retirement Income Security Act (ERISA), which governs most employer-provided LTD plans, you typically have 180 days from the date of denial to file an administrative appeal. This appeal is your opportunity to submit new and stronger medical evidence, challenge the insurer’s reasoning, and build the full record that will be used if litigation becomes necessary.

This is also where having an experienced disability insurance attorney becomes essential.

Why You Need an LTD Attorney for a Metabolic Syndrome Claim

Metabolic syndrome X claims are complex, multifaceted, and routinely underestimated by insurance companies. An experienced long-term disability attorney can:

- Review your denial letter to identify the specific grounds the insurer used and the most effective ways to challenge them

- Gather and organize your medical evidence to build the strongest possible record

- Work with medical experts to provide opinions that directly counter the insurer’s position

- Navigate ERISA’s strict procedural requirements to protect your rights at every stage

- Litigate your claim in federal court if the administrative appeal is denied

Most long-term disability attorneys work on a contingency basis — meaning you pay nothing unless they recover benefits for you. There is no financial risk to seeking a consultation.

Frequently Asked Questions About Long-Term Disability and Metabolic Syndrome X

Does metabolic syndrome X qualify for long-term disability benefits?

Yes, it can — but qualification depends on how severely the condition limits your ability to work, not on the diagnosis alone. Metabolic syndrome X is a complex, multi-system disorder involving insulin resistance, hypertension, abnormal cholesterol levels, and abdominal obesity. When these conditions combine to prevent you from performing the duties of your occupation on a sustained, full-time basis, you may be entitled to LTD benefits under your policy. The key is demonstrating functional impairment through objective medical evidence, not just the presence of a diagnosis.

Why was my long-term disability claim for metabolic syndrome denied?

The most common reasons insurers deny metabolic syndrome claims include: insufficient medical evidence, arguments that the condition is “manageable” with lifestyle changes or medication, attempts to classify symptoms like fatigue and pain as unverifiable “self-reported” conditions, and policy exclusions related to lifestyle-linked disorders. Denials are often not a reflection of the true severity of your condition — they reflect the insurer’s financial interest in avoiding a payout. A denial can and should be challenged.

How long do I have to appeal a denied LTD claim?

Under ERISA, which governs most employer-sponsored disability plans, you generally have 180 days from receiving your denial letter to file an administrative appeal. Some private (non-ERISA) policies may have different deadlines. Missing this window can permanently eliminate your right to benefits and to sue in court. If you have received a denial, you should consult with an LTD attorney as soon as possible.

What medical evidence do I need to support a metabolic syndrome disability claim?

Strong claims are built on objective, detailed documentation. This includes comprehensive lab work (lipid panels, HbA1c, fasting glucose, blood pressure records), cardiac testing results, a detailed Attending Physician Statement describing your specific functional limitations, and ideally a Functional Capacity Evaluation (FCE) that objectively measures what you can and cannot do physically. Documentation of secondary conditions — such as sleep apnea, neuropathy, or cardiovascular disease — further strengthens your case.

Can I still get disability benefits if my policy says I can do “any occupation”?

Yes, potentially. Many LTD policies shift from an “own occupation” standard (can you do your specific job?) to an “any occupation” standard after 24 months (can you do any job?). Metabolic syndrome X and its associated conditions — chronic fatigue, cardiovascular limitations, mobility impairment, cognitive difficulties — can be severe enough to prevent sustained employment in any occupation, not just your prior role. An experienced attorney can help evaluate how your policy’s definition of disability applies to your specific situation.

What if my insurer says my condition improved and terminates my benefits?

Insurers sometimes conduct periodic reviews and terminate ongoing benefits by claiming a claimant has improved sufficiently to return to work. If your benefits have been terminated on this basis, you have the right to appeal — and the same deadlines apply. It is critical to have updated medical evidence and physician support ready to counter these determinations. An LTD attorney can help you challenge a termination just as they can help with an initial denial.

Do I need a lawyer to appeal a denied long-term disability claim?

You are not legally required to hire an attorney, but having one significantly improves your chances of success — particularly under ERISA, where the administrative appeal record becomes the evidentiary foundation for any subsequent federal court lawsuit. Mistakes made during the appeal stage can be very difficult to correct later. Most LTD attorneys work on contingency, meaning you pay no fees unless they win your case.

Does metabolic syndrome X qualify for long-term disability benefits?

Why was my long-term disability claim for metabolic syndrome denied?

How long do I have to appeal a denied LTD claim?

What medical evidence do I need to support a metabolic syndrome disability claim?

Can I still get disability benefits if my policy says I can do “any occupation”?

What if my insurer says my condition improved and terminates my benefits?

Do I need a lawyer to appeal a denied long-term disability claim?

Take the Next Step Today

If your long-term disability claim for metabolic syndrome X has been denied, time is not on your side. Appeal deadlines are strict, and the longer you wait, the more difficult it can be to gather the evidence you need.

Contact our firm today for a free case review. We will examine your denial letter, evaluate your medical evidence, and give you an honest assessment of your options. You’ve already been through enough — let us fight for the benefits you’ve earned.

Sources

- Cleveland Clinic. “Metabolic Syndrome” Retrieved from (https://my.clevelandclinic.org/health/diseases/10783-metabolic-syndrome) Accessed on April 8, 2026

- Mayo Clinic. “Metabolic Syndrome” Retrieved from (https://www.mayoclinic.org/diseases-conditions/metabolic-syndrome/symptoms-causes/syc-20351916) Accessed on April 8, 2026

- Springer Nature. “Components of Metabolic Syndrome and the Risk of Disability among the Elderly Population” Retrieved from (https://www.nature.com/articles/srep22750) Accessed on April 8, 2026