Table of Contents[Hide][Show]

Founded in 1906, Reliance Standard Life Insurance Company is a member of the Tokio Marine Group, a multinational insurance holding company. Reliance Standard is a major provider of employee benefit solutions, including short- and long-term disability (LTD) insurance.

Types of Disability Coverage

Reliance Standard offers a range of disability insurance products, typically available through employers:

- Group Short-Term Disability Insurance: Provides weekly income protection, with coverage amounts up to $2,309 per week, and can replace as much as 70% of your income for up to 52 weeks.

- Group Long-Term Disability Insurance: Offers monthly income coverage of up to $24,000, with income replacement percentages ranging from 40% to 66%. Depending on the policy, benefits may be paid for 12 to 60 months, or even continue until retirement age.

- Voluntary Disability Plans: Employees may have access to voluntary short-term or long-term plans. Voluntary short-term plans can provide up to $1,250 per week, while voluntary long-term options pay up to $7,500 per month—sometimes continuing until you reach your normal Social Security retirement age.

These options are designed to help replace a portion of your income if you’re unable to work due to illness or injury.

What Is the Elimination Period for Reliance Standard’s Short-Term Disability Policy?

Most disability insurance policies include a waiting period known as the “elimination period.” This is simply the amount of time you must be unable to work due to your disability before your benefits kick in. For short-term disability, this period is typically anywhere from 7 days up to 90 days, depending on the terms set by your employer’s plan.

In other words, coverage doesn’t begin immediately after you stop working; you’ll need to satisfy this waiting period first before any payments are made. Be sure to review your specific policy for the exact length of your elimination period, as it can vary from one employer-sponsored plan to another.

K

If Reliance Standard has denied your disability claim, contact us for a free case review. A disability lawyer from our firm can review your denial letter, explain your rights, and guide you through the appeal process. If necessary, we can also help you file a lawsuit against Reliance Standard.

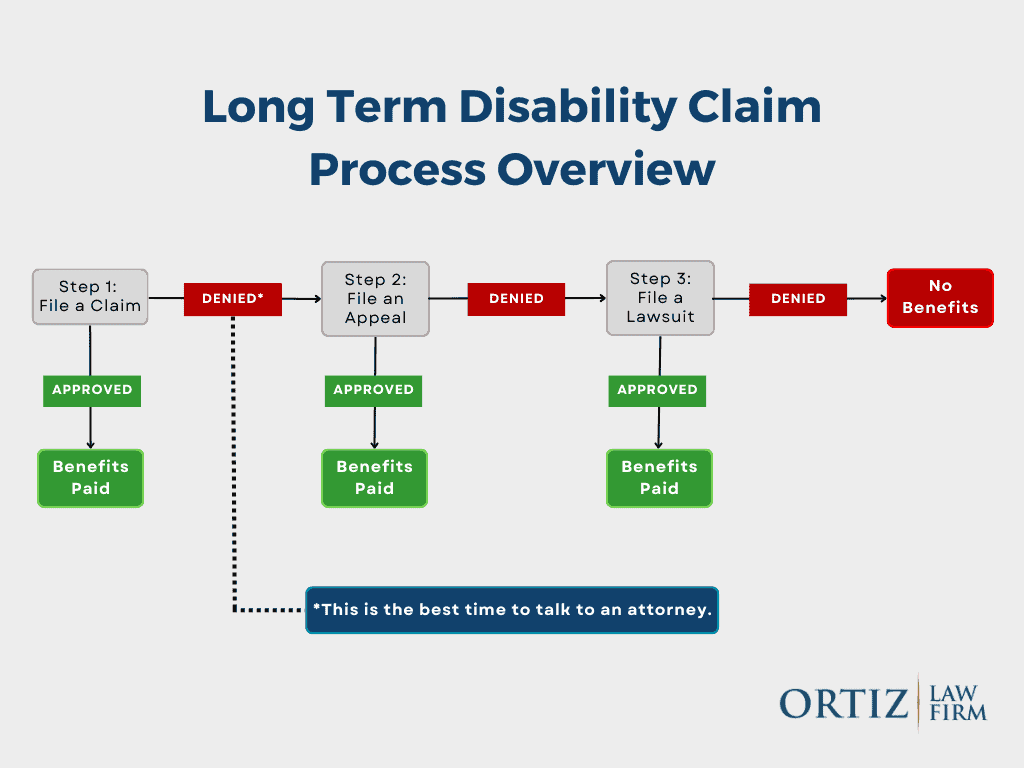

The Reliance Standard Disability Claim Review Process

Once you file a claim for Reliance Standard disability insurance benefits, a claims representative reviews your submission. During this process, Reliance Standard may request information about:

- Other disability claims you’ve filed, including SSDI

- Your activities of daily living

- Self-reported symptoms

Who Reviews Reliance Standard Disability Claims?

Initial claim reviews are typically conducted by in-house nurses employed by Reliance Standard. These reviewers evaluate your medical records, policy language, and supporting documentation to determine whether you meet the policy’s definition of disability.

If your claim is denied or terminated, Reliance Standard will issue a denial letter. These letters are often vague and conclusory, frequently stating only that you do not meet the policy’s definition of disability—without clearly identifying what evidence was missing or rejected. This lack of clarity makes the appeal process especially challenging.

Independent Medical Examinations (IME) and Functional Capacity Evaluations (FCE)

Reliance Standard may require you to attend an Independent Medical Examination (IME) or a Functional Capacity Evaluation (FCE) as part of its review.

- IME: A one-time medical evaluation performed by a physician hired and paid by the insurance company

- FCE: An assessment of physical capabilities, usually performed by a physical therapist

These exams are not conducted by your treating providers, and insurers often give them significant weight. Reliance Standard has also been known to conduct video surveillance before, during, and after these examinations, looking for activity they believe contradicts your reported limitations. Claimants should approach these exams carefully and honestly, understanding that insurers may use isolated observations to justify a denial.

It’s essential to be truthful about your symptoms and limitations—resist the temptation to exaggerate or downplay your condition. Attempting to make your case seem stronger by overstating your symptoms can backfire, as insurers are quick to label claimants as malingering if inconsistencies appear. This not only undermines your credibility but can also make appealing a denial significantly more difficult. Always be forthright during independent evaluations and with your legal counsel to give your claim the strongest foundation possible.

“Sandbagging” In Disability Insurance Claims

Reliance Standard has been known to withhold IME reports until after an appeal decision is issued. This tactic—commonly referred to as sandbagging—prevents claimants and their treating physicians from responding to unfavorable medical opinions before the record closes.

Although ERISA regulations now require insurers to disclose new evidence for claims filed after January 1, 2018, sandbagging still occurs, and claimants should watch out for this tactic.

What To Do If Reliance Standard Delays Your Disability Claim

Delays in processing your disability claim can be incredibly frustrating, especially when you need those benefits most. If you suspect Reliance Standard is dragging its feet or providing unclear updates, don’t just wait and hope for the best—take action.

First, contact your assigned claims representative to request a clear update on your claim’s status. Be sure to document every interaction—time, date, and what was discussed—for your records.

If vague answers or repeated delays continue, it may be time to seek professional help. An experienced disability attorney can spot delay tactics used by insurance companies and advocate for prompt claim processing. A lawyer can also correspond directly with Reliance Standard on your behalf, increasing your chances of a timely and thorough review.

Taking these steps early can help prevent unnecessary setbacks and move your claim forward.

Why Reliance Standard Denies Disability Insurance Claims

Long-term disability claims are frequently denied unfairly. Reliance Standard has developed a reputation for aggressive claims handling, often forcing claimants into litigation.

Common Denial Tactics

Pre-Existing Condition Limitation

Reliance Standard imposes a 3/12 pre-existing condition limitation. In plain English, if you received any treatment, consultation, care, or prescriptions for a condition in the three months before your coverage started (or before your coverage increased), you may find yourself excluded from benefits. If you become disabled from that condition within the first 12 months of being covered, the policy typically won’t pay out.

“You Do Not Meet the Definition of Disability”

Reliance Standard commonly claims that a claimant does not meet the policy’s disability definition—even in ambiguous or medically complex cases. This is especially common with conditions like long COVID, chronic pain, and fatigue-related disorders.

A Change in the Definition of Disability

After 24 months of benefits, many policies shift from an own occupation standard to any occupation. Reliance Standard frequently relies on this transition to terminate claims.

24-Month Limitation Pitfalls

Long-term disability policies typically limit benefits for mental or nervous disorders to 24 months. After those two years, continued benefits are only available if the claimant is admitted to a hospital or institution for inpatient treatment. Similarly, claims based on substance abuse are often limited to a maximum of two years, and benefits may only continue if the individual actively participates in a recognized substance abuse rehabilitation program.

These strict time limits and requirements are a common basis for denial—especially if the insurance company argues that your disabling condition falls under one of these categories, even when the medical reality is more complex. As a result, it’s not unusual for claimants with depression, anxiety, chronic pain, or substance use disorders to face early termination of benefits, regardless of ongoing symptoms or inability to work.

Other Common Policy Exclusions

Reliance Standard policies typically include a range of exclusions beyond pre-existing conditions or mental health limitations. Common scenarios that may lead to a denial include:

- Self-Inflicted Injuries: Disabilities resulting from intentional self-harm are generally not covered.

- Acts of War: Injuries or disabilities arising during acts of war, declared or undeclared, are excluded.

- Felony Activity: Disabilities sustained while committing a felony or participating in illegal activity may not be eligible for benefits.

- Elective or Cosmetic Procedures: Disabilities resulting from elective cosmetic or plastic surgery (not related to injury or illness) are often excluded.

Because policy exclusions and limitations can be nuanced and specific, it’s crucial for claimants to carefully read their plan’s terms and fully understand what is—and isn’t—covered. This knowledge can help avoid surprises during the application or appeals process.

Vague Denial Letters

Denial letters often lack meaningful explanations, forcing claimants to guess what evidence is needed to appeal.

How to Strengthen Your Disability Claim

Meet Your Policy’s Definition of Disability

Disability is defined by your insurance policy—not by statute. Many Reliance Standard policies require:

- Inability to perform your own occupation for the first 24 months

- Inability to perform any occupation thereafter

Limitations on mental or nervous disorder claims are common. Understanding your exact policy language is critical.

Submit Comprehensive Medical Evidence

Claims reviewers may selectively cite records to support denial. Protect yourself by submitting:

- Complete medical records

- Diagnostic testing (MRI, CT, etc.)

- Detailed physician opinions describing functional limitations

Be Prepared for Surveillance

Reliance Standard frequently uses private investigators and social media monitoring. A brief moment of activity on a “good day” does not mean you can work full time—but insurers often argue otherwise.

The Reliance Standard Appeals Process

If your claim is denied, the next step is an administrative appeal. During the appeal, Reliance Standard may rely on third-party file reviewers or require additional IMEs or FCEs.

Because courts generally cannot consider new evidence later, the appeal stage is your most important opportunity to build the administrative record.

How Does ERISA Affect Reliance Standard Disability Claims?

Most employer-sponsored disability plans are governed by ERISA, a federal law that strongly favors insurers.

Under ERISA:

- You usually have 180 days to appeal

- Courts review only the evidence submitted during the appeal

- Missing evidence can permanently harm your case

Recent ERISA rule changes now require insurers to disclose new evidence before issuing a final decision—but only for claims filed on or after January 1, 2018.

Lawsuits Against Reliance Standard

If your appeal is denied—or if you have an individual policy not governed by ERISA—you may be able to file a lawsuit. Reliance Standard has dedicated ERISA litigation teams, so it is critical that you involve legal help early.

How the Ortiz Law Firm Can Help with Your Claim

If you are preparing to file a claim for long-term disability benefits, our Disability Insurance Claim Guide and Toolkit will guide you through the process and help you gather the information you need to support your claim.

We also have a free eBook called “The Top Ten Mistakes That Will Destroy Your Long-Term Disability Claim“ that can help you avoid common mistakes that could destroy your claim.

How Can a Lawyer Help After a Denial?

When your insurance company refuses to pay your disability benefits, an experienced ERISA attorney like those at the Ortiz Law Firm can:

- Review your policy and determine whether ERISA applies

- Obtain and analyze your complete claim file

- Identify weaknesses in the insurer’s reasoning

- Gather additional medical and vocational evidence

- Prepare a comprehensive appeal

- File suit if benefits are still denied

Many of the Reliance Standard appeals that we handle result in the claim being reinstated. We work on a contingency fee basis, meaning you pay nothing unless benefits are recovered.

Get Help With Your Reliance Standard Disability Claim

If Reliance Standard is denying your long-term disability benefits, the Ortiz Law Firm can help. Disability attorney Nick Ortiz represents claimants nationwide.

Call us at (888) 321-8131 to request a free consultation today.